Who helps reduce the financial burden of being hospitalised?

News Article

Publication date:

10 April 2019

Last updated:

25 February 2025

Author(s):

Joshua Jinks

When clients are spending a prolonged amount of time in the hospital either for themselves or their children, the last thing they want to think about is the financial impact on their family.

The immediate costs of being at the hospital can build up and create unwanted stress. In this week’s insights, we look at how hospitalisation benefit can help cover some of these costs and allow them to focus on their, or in some cases their children’s health.

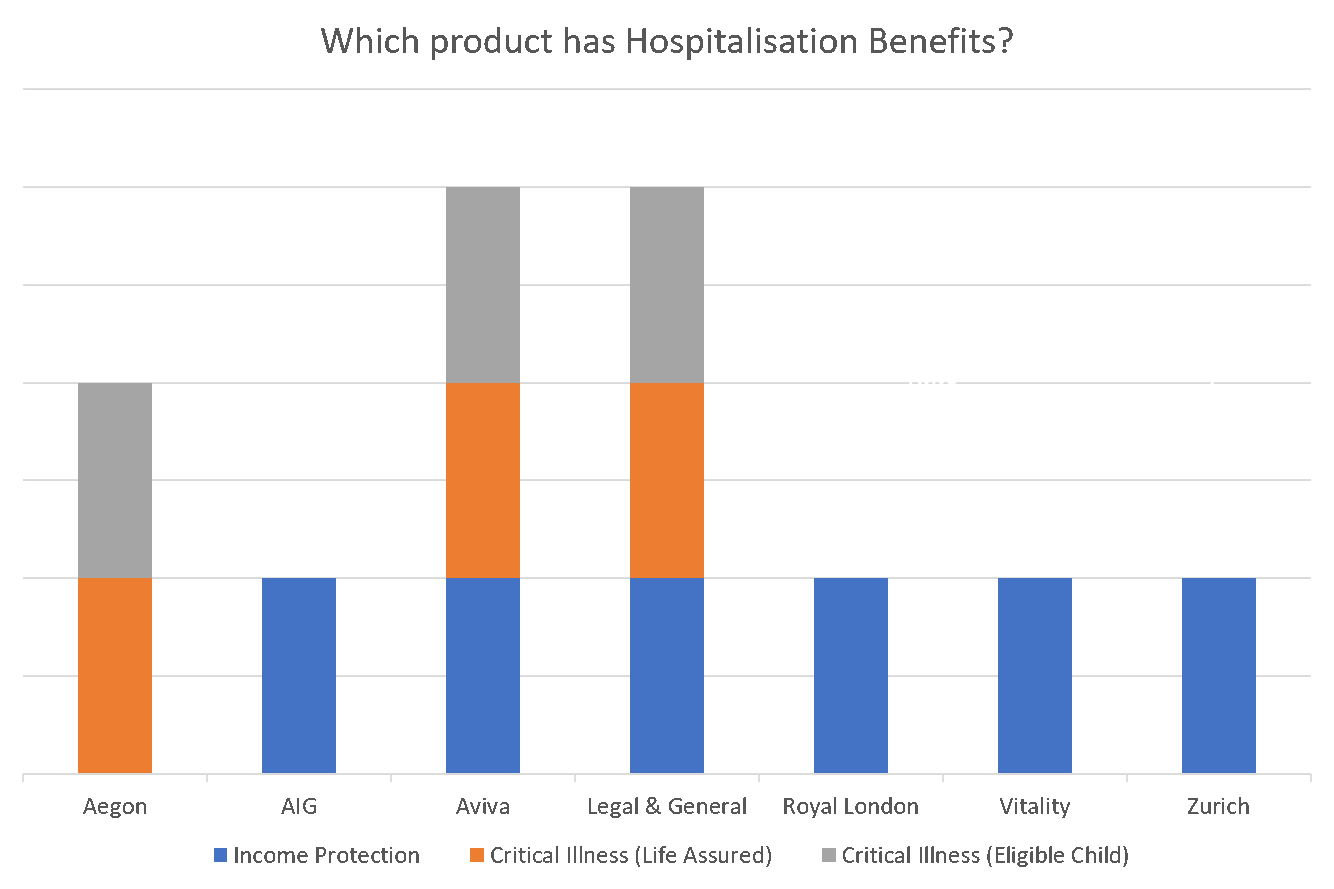

Hospitalisation benefits provided by AIG, Aviva, Royal London, Vitality Life (comprehensive only), Zurich (select only) and Legal & General are designed to ease such financial concerns by providing a pay out if the life assured or an eligible child is hospitalised for an extended period of time within their deferred period.

Historically, hospitalisation benefits have been offered only through income protection plans. In recent times however, a number of insurers have extended the offering into their critical illness propositions where often both the life assured and their children are covered.

The payments can be used in any way the client requires, but can be of great assistance in helping both the life assured and their family meet the costs of being hospitalised. Examples of these costs include:

- Hospital parking

- Travel to and from the hospital

- Hotel stays

- Childcare

- Unpaid leave from work

Whilst not all of these costs are likely to apply to any one person, each of them could lead to increasing costs being placed on the life assured and family which could be eased if hospitalisation benefit was included in their Protection plan.

For a successful claim to be made the life assured needs to have spent a number of successive nights within a hospital, after which the insurer will pay a set amount for each subsequent night they remain hospitalised. Legal & General, Vitality and Zurich require the life assured to have spent 7 consecutive nights in hospital, however AIG, Aviva and Royal London offer slightly better terms and will start payments after 6 consecutive nights.

In the case of AIG, Aviva, Royal London, Vitality and Zurich the hospitalisation payment is a flat amount of £100.00 per night. In comparison, Legal & General will pay one thirtieth (1/30) of the monthly benefit.

In real terms, this means that any client with a sum assured of up to £3,000 per month would be better off if they took out an AIG, Aviva, Royal London or Zurich plan. At £3,000 all four will pay the same, however where a client has a sum assured greater than £3,000 per month, that client would receive more from Legal & General with the amount they will pay per night capped at £150.

Each insurer will pay the hospitalisation benefit as a lump sum and the maximum they will pay is dependent on a number of factors:

- The length of the deferred period – As this benefit is only available during the deferred period it will cease if and when the deferred period ends and the plan goes into full payment.

- The client being discharged from hospital – If the client is discharged from hospital then each insurer will cease the hospitalisation benefit. If they are required to subsequently return to hospital at a later date the benefit can start again after the initial period of consecutive time spent in hospital is completed.

- The period of time defined by the insurer – AIG, Aviva, Royal London, Vitality and Zurich will pay the hospitalisation benefit for 90 nights, whilst Legal & General go one night further by ceasing payments after 91 nights.

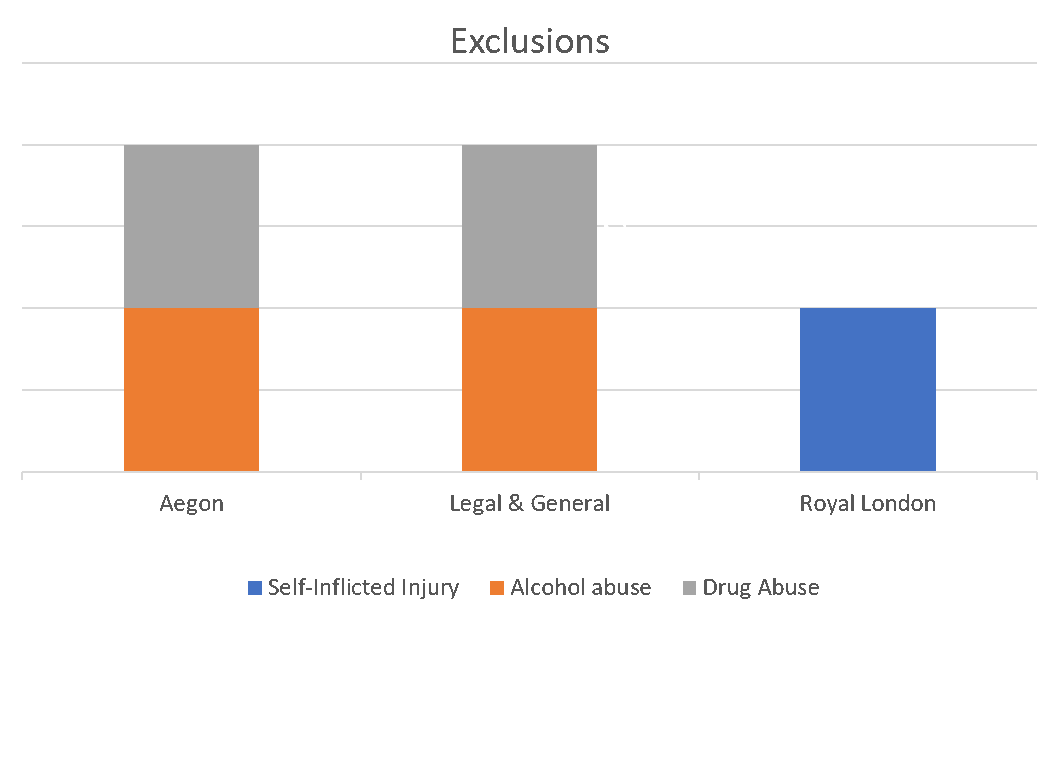

AIG, Vitality, Zurich and Aviva do not apply any exclusions to their hospitalisation benefits whereas Royal London apply an exclusion if hospitalisation is due to intentional self-inflicted injury. On the other hand, Aegon and Legal & General apply exclusions as a direct result of either alcohol or drug abuse.

Whilst the hospitalisation benefit is provided with the aim of helping clients meet the costs of being hospitalised, it can also help inform insurers of the client’s condition sooner. This can allow the insurer to be proactive in offering other non-financial benefits they may provide (such as occupational therapy, physiotherapy or other complimentary therapies) to help the client return to work faster. These are frequently referred to as early intervention.

In many cases this may mean the client can return to work before the end of the deferred period. An early return to work can significantly reduce the long-term impact of an absence on an individual’s career. While this can reduce the cost of claims to insurers, this will normally involve them in some expense. The important thing from the client point of view however, is that they can return to work sooner and reduce the disruption of their career. In 2015, 80% of mental health absences reported to Legal & General resulted in a return to work before becoming a claim as a result of early treatment. Whilst it may not be suitable for all clients, for others it may help reduce financial stress in a period when Income Protection plans generally offer little financial support.

Each provider offering hospitalisation benefit have different benefits and overall each proposition seems strong in different areas. For clients with higher benefit amounts Legal & General may pay more on a day to day basis, however the shorter waiting period offered by AIG and Aviva means that a client would be required to have an extended period in hospital in order to receive more overall.

To sign up to the F&TRC mailing list you can register your details here.

This document is believed to be accurate but is not intended as a basis of knowledge upon which advice can be given. Neither the author (personal or corporate), the CII group, local institute or Society, or any of the officers or employees of those organisations accept any responsibility for any loss occasioned to any person acting or refraining from action as a result of the data or opinions included in this material. Opinions expressed are those of the author or authors and not necessarily those of the CII group, local institutes, or Societies.