Investment planning update: UK gilt yield drop

Technical article

Publication date:

02 June 2020

Last updated:

25 February 2025

Author(s):

Technical Connection

Update from 14 May 2020 to 27 May 2020

Investment planning update: UK gilt yield drop

UK gilt yield drop

(AF4, FA7, LP2, RO2)

While the focus has been on gyrating share indices, something interesting has been happening in the UK gilts market.

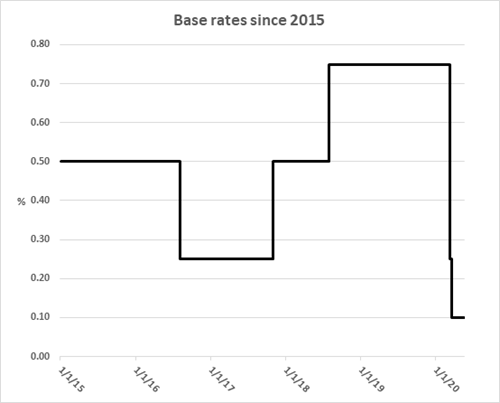

May 20 was a momentous day for the UK gilts market.

The Debt Management Office (DMO), the Treasury arm charged with the ever more Herculean task of selling government debt, sold £3.8bn worth of gilts at a negative yield. The stock concerned was 0¾% Treasury 2023 and the average yield at which it was sold was -0.003%. £3.75bn nominal of the stock was offered to the market and the DMO received bids for £8.073bn, so there was no shortage of market interest (sic).

The fact that large investors were willing to buy, safe in the knowledge that they would lose money if they held the gilt to its January 2023 redemption date, says much about the expectations for future interest rates. At the weekend, the Bank of England’s chief economist, Andy Haldane, told the Sunday Telegraph that the Bank was looking at negative rates. Yesterday Andy’s boss, the Governor of the Bank of England, Andrew Bailey, was asked about negative rates by MPs on the House of Commons Treasury Select Committee. He responded, in a manner typical of central bankers, by saying “We do not rule things out as a matter of principle, that would be, I think, a foolish thing to do.” His reply was widely seen as a watering down of the Bank’s previous position under Mark Carney, where the Old Lady turned its face against sub-zero rates.

Were the UK to opt for negative interest rates, it would be joining the Eurozone, Japan and Switzerland in the Alice in Wonderland world where large borrowers get paid by institutional lenders. At the retail level, the experience has been that bank deposit rates tend to stick at 0%, except for large sums, and mortgages are, alas, not a way of earning interest for homeowners.

Whether negative rates work is a point that is still being argued about. The theory is that if the banks are penalised for holding reserves with the central bank, they will be more encouraged to lend to businesses and thereby stimulate the economy. The proof is less obvious – just consider the Eurozone and Japanese economies.

Interestingly, a pioneer of negative rates, Sweden, has recently increased its rates to 0%, unconvinced about the sub-zero wisdom. There is a danger that, as individuals try to rebuild their savings after the pandemic, a lack of interest will simply make them save more and spend less – the opposite of what the economy needs.

The Bank of England’s next Monetary Policy Committee meeting is on 18 June, although in current market conditions, that does not mean a rate announcement will not be made earlier.

Source: DMO 20/5/20

This document is believed to be accurate but is not intended as a basis of knowledge upon which advice can be given. Neither the author (personal or corporate), the CII group, local institute or Society, or any of the officers or employees of those organisations accept any responsibility for any loss occasioned to any person acting or refraining from action as a result of the data or opinions included in this material. Opinions expressed are those of the author or authors and not necessarily those of the CII group, local institutes, or Societies.